Firms in low- and middle-income countries (LMICs) have been shown to “upgrade” – a term capturing innovation, but also simpler decisions that raise firms’ productivity such as adopting products or technologies that were already invented elsewhere. This is often viewed as a puzzle because upgrading should be easier for firms that use outdated processes or technologies, yet many such firms in developing countries upgrade less. Limited firm upgrading slows economic growth because it prevents firms from expanding and becoming more productive.

This paper asks whether small firms in developing countries are risk averse, preventing them from engaging in experimentation that is necessary to grow. The prevailing view of firms in high-income settings is that they are risk neutral because investors in firms have diversified portfolios. In practice, this means that enterprises will pursue investments with positive average returns even if they are risky. But the modal firm in low and middle-income countries is small and owner-operated, meaning that business losses may directly impact owners’ consumption. This may deter small firms from pursuing high average return but uncertain investments, constraining growth.

My job market paper tests this hypothesis in the context of one of the simplest upgrading decisions: retail firms’ decision to stock and sell a new consumer product. Retail is one of the most common firm types in LMICs and offering new products is among the simplest, yes most consequential, forms of technology adoption that such firms may engage in. I posit that offering new products is risky because firms don’t know if their customers will demand the good at the time when they invest in stock.

Using two field experiments with over 1,200 Kenyan retailers, I find that reducing business risk—through insurance or learning—dramatically increases investment, consistent with the idea that owner-operators’ personal risk preferences can constrain firm growth. I then show that this lack of experimentation prevents firms from learning about product profitability in the longer run: retailers temporarily shielded from the risk of stocking a new product went on to permanently stock it at a higher rate.

In 2020, a Kenyan motorcycle importer constructed a new factory to produce effective motorcycle helmets near Nairobi. The factory produces one of the first helmets that complies with Kenya’s helmet safety standards while still being affordable to a typical household. Yet retail adoption was slow: although more than half of nearby shops believed selling helmets would be profitable, under 6% stocked them two years after the factory was opened.

Descriptive evidence suggests that firm risk aversion may explain this mismatch: shops were particularly unlikely to stock helmets if they reported uncertain beliefs about the profitability of helmets. I implemented two field experiments to test if risk aversion affects small firms’ stocking decisions and prevents them from engaging in experimentation required to discover profitable new products.

Experiment 1: Are Firms Risk Averse?

The first experiment, the Insurance Experiment, directly tested whether firms behave as if they are risk averse. I offered 350 small retailers in western Kenya the chance to buy helmet stock either with or without an insurance contract. If firms purchased helmet stock and then failed to sell out, they received a payment to offset some of their losses. The contract was designed to lower average profits but also lower risk, meaning that it is only attractive to a risk averse firm.

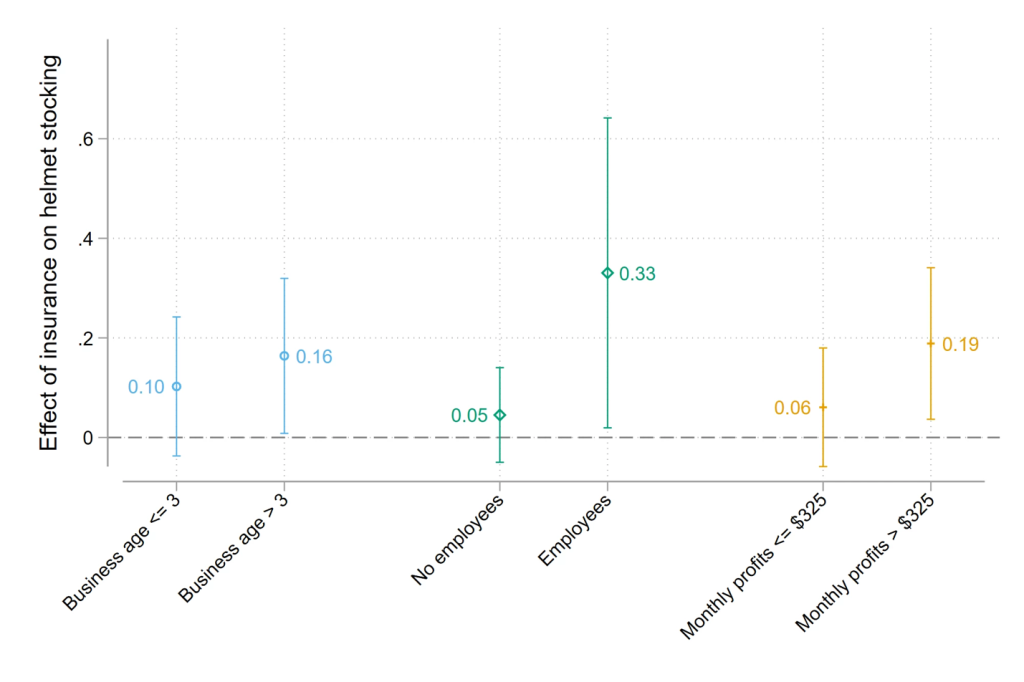

If firms were risk neutral, insurance shouldn’t matter. Yet insurance increased stocking by 50% (10 percentage points), with the largest effects among shops whose owners demonstrated high risk aversion. For comparison, only 30% of firms had tried stocking any new product in the past year. The results were not driven by new or struggling firms: longer tenured and more profitable enterprises exhibited larger responses to the insurance contract. This is likely explained by the fact that, unlike the smallest firms, they had resources available to purchase helmet stock, yet many such firms were unwilling to make the investment absent protection from risk. This is important to policy, as it indicates that just giving firms cash may not induce them to invest in the most profitable opportunities unless they are also insured against risk.

Figure 1: Effects of insurance on helmet stocking rate by firm age and size

Experiment 2: Does risk aversion slow the adoption of profitable goods?

The Insurance Experiment indicates that risk aversion affects firms’ stocking decisions. Is this because helmets are new or because their demand is truly volatile? And does this matter for longer-run productivity? The second experiment, the Learning Experiment, followed 929 Nairobi retailers who had access to stock of the helmets for more than two years yet had chosen not to try stocking them. I offered two randomly assigned treatments to test if risk aversion prevents retailers from engaging in new product experimentation required to learn about profitable new goods.

In the first treatment, I temporarily offered some shops a buyback policy: they could return unsold helmets for a refund. During this first phase, adoption jumped from 6.8% to 16.4%, a 240% increase.

The more striking result is that this one-time change led to greater permanent adoption. Once the return option expired and all firms faced the same risk, the previously treated shops remained 70% more likely to stock helmets. They had learned that the product was profitable—and kept selling it. Firms reported that this helped them expand their business profitability: with the average adopter reporting that selling helmets made their shop about 10% more profitable by the endline survey, with most firms reporting plans to expand how much they stock.

In a second experimental arm, the supplier commitment, I argue that these results are not consistent with firms simply failing to internalize the value of learning into their investment decisions. The treatment raised the value of learning without affecting short-run profits. I committed to help treated shops restock from the supplier when the study ended (many expressed concerns that they would be unable to do so without help), ensuring that shops could continue selling helmets if they found them profitable. This increase in the future value of information increased upfront stocking by 80%, showing that low helmet experimentation was not simply a result of firm myopia.

Another possible story is that shops could have simply underestimated helmet profitability. But I show that the beliefs of shops induced to try stocking by the return policy were optimistic but uncertain, and experience in the market resolved their uncertainty about profitability but did not change mean profit expectations.

Taken together, these results suggest that the return policy caused shops deterred from trying to stock helmets by risk aversion to experiment, who then overcame uncertainty with experience and no longer viewed stocking as risky. The results indicate a permanent change in the production function of complying retailers that helped them grow.

The Big Picture: A Manufacturer’s Dilemma

The most consequential takeaway isn't just for the retailers—it's for the manufacturers. If retailers are too risk averse to experiment, the total market size for new goods shrinks. This lowers the incentive for manufacturers to innovate or introduce products specifically for LMIC contexts, creating a cycle of slow technological progress.

About the Author

Grady Killeen is an economics PhD candidate at UC Berkeley.

He studies economic development, with a focus on topics from industrial organization, entrepreneurship, and applied econometrics. To learn more about his work, visit his website: https://gkilleen33.github.io/